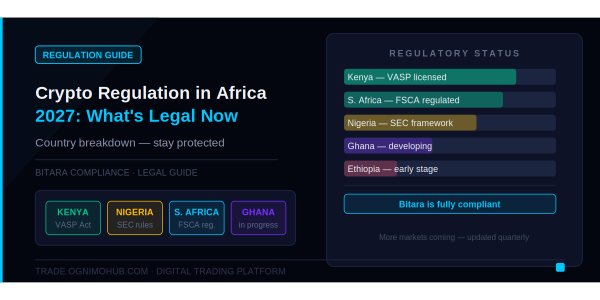

Crypto Regulation in Africa in 2027: What's Legal, What's Changing, and How to Stay Protected

By Bitara Compliance · Legal Guide · May 2026 · 10 min read

Why Regulation Matters More Than the Price Chart

For most crypto traders, regulatory news is background noise. A headline about a licensing framework in South Africa or a VASP bill in Kenya does not move the ticker the way a BTC price action does.

This is a mistake. Regulatory clarity — or its absence — determines which platforms can operate, which payment rails are accessible, how user funds are protected, and whether institutional capital flows into your market. Understanding the regulatory landscape in your country is not a compliance formality. It is material information for your trading strategy.

In 2026, Africa is in the middle of the most significant regulatory transformation in its crypto history. This post gives you a country-by-country breakdown of where things stand, where they are heading, and what it means for your trading on Bitara.

South Africa: Africa's Regulatory Blueprint

South Africa has emerged as one of the continent's early leaders in crypto regulation, and its framework is increasingly being used as a model for other African jurisdictions.

Beginning in June 2023, the country implemented a comprehensive framework classifying crypto assets as financial products. Under this regime, Crypto Asset Service Providers (CASPs) must obtain licenses and comply with oversight from the Financial Sector Conduct Authority (FSCA) and the Financial Intelligence Centre.

By March 2024, South Africa had approved 59 crypto operating licenses. The intergovernmental fintech working group is actively refining regulations and plans to formally classify stablecoins as a distinct subset of crypto assets — which would be one of the first such regulatory classifications in Africa.

What this means for traders: South Africa is the continent's most regulated crypto environment, which cuts both ways. Licensed platforms operating in South Africa provide stronger user protections and are less vulnerable to sudden regulatory shutdowns. But the compliance requirements also filter out less reputable operators, which is ultimately protective for users.

Bitara status in South Africa: Operating under FSCA compliance frameworks with full KYC/AML procedures.

Nigeria: Turbulence to Regulation — The Long Journey

Nigeria's regulatory journey has been the continent's most turbulent. The Central Bank of Nigeria initially restricting bank involvement in cryptocurrency transactions in 2021, before gradually softening its stance. The push-pull between the CBN and the SEC created an environment where crypto usage flourished despite (not because of) the regulatory framework.

By 2026, the Securities and Exchange Commission has issued 25 virtual asset licenses under a regulatory sandbox model, signalling a fundamental shift in posture. Nigeria is no longer trying to stop crypto — it is building the infrastructure to regulate and tax it.

The remaining friction is at the banking interface. Converting significant volumes of naira to crypto and back remains operationally complex, which is precisely why P2P trading has become so dominant in Nigeria. Traders bypass the bank interface entirely, transacting directly with counterparties.

What this means for traders: P2P remains the primary on-ramp in Nigeria. Using licensed, regulated P2P platforms like Bitara provides legal protection and dispute resolution mechanisms that informal Telegram and WhatsApp group trades do not. The regulatory trend is toward increasing formalisation — traders who have operated on regulated platforms will be better positioned as the framework matures.

Kenya: The VASP Framework Arrives

Kenya edged toward formal crypto regulation in 2025 when its parliament passed a Virtual Asset Service Provider (VASP) bill establishing a licensing framework. This represents Kenya's first substantive move from an essentially unregulated posture toward a structured oversight regime. A nationwide consultation on the drafted regulations is currently underway.

Kenya's framework is expected to require exchanges to register with the Capital Markets Authority, implement KYC/AML procedures, and maintain segregated client funds. The framework draws heavily on international standards from the Financial Action Task Force (FATF).

The absence of explicit prohibition prior to the VASP bill had allowed both local and international platforms to operate, though operators faced uncertainty regarding long-term regulatory expectations. The new framework resolves that uncertainty — exchanges that register and comply will have clear legal standing.

What this means for traders: The VASP framework in Kenya is constructive for crypto. It does not restrict trading — it legitimises it. Licensed platforms will be able to integrate with Kenyan banking infrastructure more directly, potentially enabling M-Pesa on-ramps that are currently available only through P2P channels.

Ghana: Emerging Regulation, Strong Fundamentals

Ghana now requires virtual asset providers to register ahead of broader guidance — an intermediate step toward full licensing that signals regulatory intent without yet specifying comprehensive requirements.

The Bank of Ghana has taken a more measured approach than Nigeria's CBN, neither restricting crypto activity nor formally accommodating it, while the registration requirement establishes a preliminary record of which operators are active in the market.

Ghana's position in 2026 is pre-formal-regulation but with clear direction toward it. Operators registered under the interim requirement are better positioned when comprehensive rules arrive.

What this means for traders: Ghana is a growing market with constructive regulatory momentum. Trading through licensed and registered platforms provides better recourse than informal channels, and the regulatory trajectory points toward increased protection over the next 12–24 months.

Mauritius: The Regional Regulatory Leader

Mauritius introduced one of Africa's earliest comprehensive frameworks through the VAITOS Act of 2021. The Financial Services Commission licenses providers across broker-dealer, custodian, and marketplace categories. The island issued stablecoin guidance in 2025 and is now developing a broader stablecoin framework.

Mauritius serves as a regulatory reference for other African jurisdictions and has positioned itself as the continent's fintech compliance hub — the Singapore of African crypto regulation.

What All Traders Should Know in 2026

KYC is not optional — and that is a good thing. Know Your Customer requirements protect users by ensuring platforms have verified counterparty information. When disputes arise in P2P trading, KYC records provide the documentation needed for resolution. Platforms that avoid KYC are often avoiding it because they cannot pass the regulatory requirements — which is a risk signal, not a feature.

Segregated funds matter. Regulatory frameworks require licensed platforms to hold user funds separately from operational capital. This protects you if the platform encounters financial difficulties. When using any crypto platform, verify whether it is licensed in your jurisdiction and whether it maintains segregated client funds.

Stablecoin regulation is coming. Multiple African regulators are developing specific stablecoin frameworks. This will formalise USDT and USDC usage in cross-border trade and remittances — and will likely require regulated stablecoin service providers to obtain specific licenses. This is a tailwind for regulated platforms like Bitara, which are already operating within compliance frameworks.

P2P escrow provides legal recourse. Bitara's P2P marketplace uses escrow — funds are held by the platform until both parties confirm the transaction. This is critically important in markets where informal P2P trades through messaging groups have no dispute resolution mechanism. Escrow-based P2P on a regulated platform is the standard that regulatory frameworks are moving toward.

The 2027 Outlook

Regulatory collaboration is emerging across the region. Refined frameworks in influential economies like South Africa, Nigeria and Kenya could serve as models for other nations. Cross-border fintech initiatives and collaboration are creating a more harmonized overall ecosystem.

2026 and 2027 are shaping up to be watershed years for several African jurisdictions. The trajectory is clear: regulated, licensed, compliant platforms will increasingly have access to banking infrastructure, institutional capital, and the trust of a growing middle class that is cautious about fraud and platform failures.

Bitara's compliance-first approach is not a limitation. It is the infrastructure for the next phase of African crypto growth.

Share This Post

By Bitara Compliance · Legal Guide · May 2026 · 10 min read

Why Regulation Matters More Than the Price Chart

For most crypto traders, regulatory news is background noise. A headline about a licensing framework in South Africa or a VASP bill in Kenya does not move the ticker the way a BTC price action does.

This is a mistake. Regulatory clarity — or its absence — determines which platforms can operate, which payment rails are accessible, how user funds are protected, and whether institutional capital flows into your market. Understanding the regulatory landscape in your country is not a compliance formality. It is material information for your trading strategy.

In 2026, Africa is in the middle of the most significant regulatory transformation in its crypto history. This post gives you a country-by-country breakdown of where things stand, where they are heading, and what it means for your trading on Bitara.

South Africa: Africa's Regulatory Blueprint

South Africa has emerged as one of the continent's early leaders in crypto regulation, and its framework is increasingly being used as a model for other African jurisdictions.

Beginning in June 2023, the country implemented a comprehensive framework classifying crypto assets as financial products. Under this regime, Crypto Asset Service Providers (CASPs) must obtain licenses and comply with oversight from the Financial Sector Conduct Authority (FSCA) and the Financial Intelligence Centre.

By March 2024, South Africa had approved 59 crypto operating licenses. The intergovernmental fintech working group is actively refining regulations and plans to formally classify stablecoins as a distinct subset of crypto assets — which would be one of the first such regulatory classifications in Africa.

What this means for traders: South Africa is the continent's most regulated crypto environment, which cuts both ways. Licensed platforms operating in South Africa provide stronger user protections and are less vulnerable to sudden regulatory shutdowns. But the compliance requirements also filter out less reputable operators, which is ultimately protective for users.

Bitara status in South Africa: Operating under FSCA compliance frameworks with full KYC/AML procedures.

Nigeria: Turbulence to Regulation — The Long Journey

Nigeria's regulatory journey has been the continent's most turbulent. The Central Bank of Nigeria initially restricting bank involvement in cryptocurrency transactions in 2021, before gradually softening its stance. The push-pull between the CBN and the SEC created an environment where crypto usage flourished despite (not because of) the regulatory framework.

By 2026, the Securities and Exchange Commission has issued 25 virtual asset licenses under a regulatory sandbox model, signalling a fundamental shift in posture. Nigeria is no longer trying to stop crypto — it is building the infrastructure to regulate and tax it.

The remaining friction is at the banking interface. Converting significant volumes of naira to crypto and back remains operationally complex, which is precisely why P2P trading has become so dominant in Nigeria. Traders bypass the bank interface entirely, transacting directly with counterparties.

What this means for traders: P2P remains the primary on-ramp in Nigeria. Using licensed, regulated P2P platforms like Bitara provides legal protection and dispute resolution mechanisms that informal Telegram and WhatsApp group trades do not. The regulatory trend is toward increasing formalisation — traders who have operated on regulated platforms will be better positioned as the framework matures.

Kenya: The VASP Framework Arrives

Kenya edged toward formal crypto regulation in 2025 when its parliament passed a Virtual Asset Service Provider (VASP) bill establishing a licensing framework. This represents Kenya's first substantive move from an essentially unregulated posture toward a structured oversight regime. A nationwide consultation on the drafted regulations is currently underway.

Kenya's framework is expected to require exchanges to register with the Capital Markets Authority, implement KYC/AML procedures, and maintain segregated client funds. The framework draws heavily on international standards from the Financial Action Task Force (FATF).

The absence of explicit prohibition prior to the VASP bill had allowed both local and international platforms to operate, though operators faced uncertainty regarding long-term regulatory expectations. The new framework resolves that uncertainty — exchanges that register and comply will have clear legal standing.

What this means for traders: The VASP framework in Kenya is constructive for crypto. It does not restrict trading — it legitimises it. Licensed platforms will be able to integrate with Kenyan banking infrastructure more directly, potentially enabling M-Pesa on-ramps that are currently available only through P2P channels.

Ghana: Emerging Regulation, Strong Fundamentals

Ghana now requires virtual asset providers to register ahead of broader guidance — an intermediate step toward full licensing that signals regulatory intent without yet specifying comprehensive requirements.

The Bank of Ghana has taken a more measured approach than Nigeria's CBN, neither restricting crypto activity nor formally accommodating it, while the registration requirement establishes a preliminary record of which operators are active in the market.

Ghana's position in 2026 is pre-formal-regulation but with clear direction toward it. Operators registered under the interim requirement are better positioned when comprehensive rules arrive.

What this means for traders: Ghana is a growing market with constructive regulatory momentum. Trading through licensed and registered platforms provides better recourse than informal channels, and the regulatory trajectory points toward increased protection over the next 12–24 months.

Mauritius: The Regional Regulatory Leader

Mauritius introduced one of Africa's earliest comprehensive frameworks through the VAITOS Act of 2021. The Financial Services Commission licenses providers across broker-dealer, custodian, and marketplace categories. The island issued stablecoin guidance in 2025 and is now developing a broader stablecoin framework.

Mauritius serves as a regulatory reference for other African jurisdictions and has positioned itself as the continent's fintech compliance hub — the Singapore of African crypto regulation.

What All Traders Should Know in 2026

KYC is not optional — and that is a good thing. Know Your Customer requirements protect users by ensuring platforms have verified counterparty information. When disputes arise in P2P trading, KYC records provide the documentation needed for resolution. Platforms that avoid KYC are often avoiding it because they cannot pass the regulatory requirements — which is a risk signal, not a feature.

Segregated funds matter. Regulatory frameworks require licensed platforms to hold user funds separately from operational capital. This protects you if the platform encounters financial difficulties. When using any crypto platform, verify whether it is licensed in your jurisdiction and whether it maintains segregated client funds.

Stablecoin regulation is coming. Multiple African regulators are developing specific stablecoin frameworks. This will formalise USDT and USDC usage in cross-border trade and remittances — and will likely require regulated stablecoin service providers to obtain specific licenses. This is a tailwind for regulated platforms like Bitara, which are already operating within compliance frameworks.

P2P escrow provides legal recourse. Bitara's P2P marketplace uses escrow — funds are held by the platform until both parties confirm the transaction. This is critically important in markets where informal P2P trades through messaging groups have no dispute resolution mechanism. Escrow-based P2P on a regulated platform is the standard that regulatory frameworks are moving toward.

The 2027 Outlook

Regulatory collaboration is emerging across the region. Refined frameworks in influential economies like South Africa, Nigeria and Kenya could serve as models for other nations. Cross-border fintech initiatives and collaboration are creating a more harmonized overall ecosystem.

2026 and 2027 are shaping up to be watershed years for several African jurisdictions. The trajectory is clear: regulated, licensed, compliant platforms will increasingly have access to banking infrastructure, institutional capital, and the trust of a growing middle class that is cautious about fraud and platform failures.

Bitara's compliance-first approach is not a limitation. It is the infrastructure for the next phase of African crypto growth.